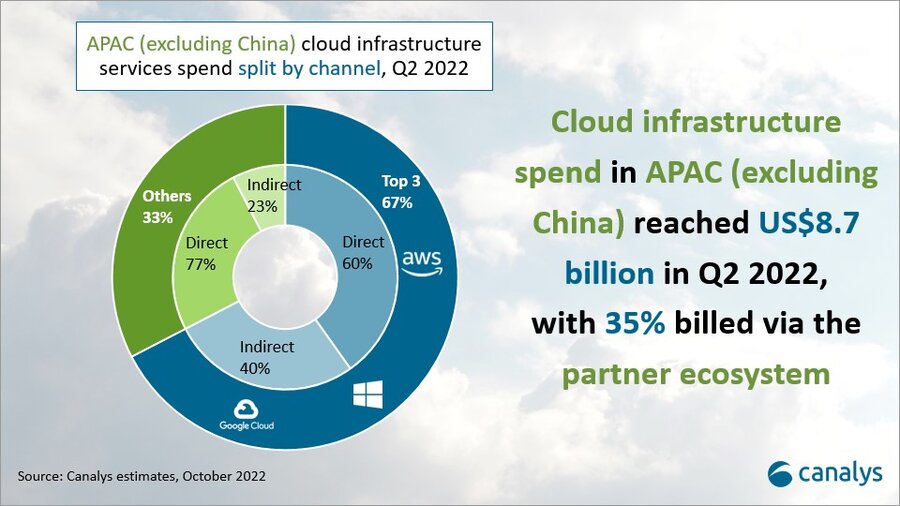

Cloud infrastructure services spend in the Asia Pacific region (excluding China) reached US$8.7 billion in Q2 2022, up 35% and accounting for 14% of worldwide cloud spend. Amazon Web Services (AWS) and Microsoft Azure are the clear leaders in the region’s cloud market. The acceleration of digital transformation has brought tremendous demand for cloud in APAC. Small and medium-sized business cloud spend is set to increase and will be a major driver of cloud market growth in the coming year. Channel partners, which provide the most reach into SMBs in the region, will be key to winning and retaining customers in the future. Most of the major cloud providers in APAC are investing in channel growth and recruitment.

Asia Pacific’s cloud market is complex, with varying levels of maturity

Demand for cloud services remains strong in APAC, driven by governments’ digitalization efforts and companies’ desire to future-proof to ensure business continuity. APAC now accounts for 14% of global cloud spend, and the region’s cloud market continues to grow rapidly.

Because of the varying levels of cloud maturity and readiness, and the differences in regulatory requirements and localization needs, navigating the APAC cloud market is difficult. Cloud partners play an increasingly important role in cloud adoption as they help remove barriers and lower the cost of entering new markets. Marketplaces are also developing as a key route to market – cloud provider marketplaces are in place to attract ISVs and drive cloud use, while distributor marketplaces support automation of cloud and SaaS delivery and help cloud vendors reach new partner types.

AWS and Microsoft Azure lead the Asia Pacific cloud market

- Amazon Web Services (AWS) was the leading cloud service provider in Q2 2022, accounting for 32% of the market. Its indirect business is small compared with its direct business. But its indirect business is growing at a much faster rate. It announced new investments in APN Programs and Training Units (AWS certifications), to support its partners in the key areas of cultivating technical talent and ramping up sales.

- Microsoft Azure came second in Q2 2022, with a 26% market share. Azure is entrenched in the channel and has by far the most extensive reach in the SMB market. More than half of its APAC revenue comes from the channel, and Microsoft plans to continue investing in the partner ecosystem to sustain its momentum with its new Cloud Partner Program, which focuses on accelerating the Azure business through partners.

- Google Cloud accounted for 9% of the APAC market. It is extending its reach into distribution, signing a partnership with Ingram Micro in Southeast Asia this quarter to drive into SMB channels. It continues to prioritize a vertical-led go-to-market strategy, targeting partners that can align with these plans. Google Cloud CEO Thomas Kurian has highlighted his commitment to reach 100% partner attachment in every Google Cloud deal.

- Other cloud providers accounted for the remaining 33% of the market, with much fewer indirect sales than the top three. Cloud providers such as Alibaba Cloud, Huawei Cloud and Tencent Cloud are looking to accelerate their expansion into Southeast Asia, launching new data center regions and winning large deals to grow their presence in the sub-region. Some plan to leverage the APAC channel as a key route to market, but strong channel programs and channel strategies are yet to be seen.

“Microsoft Azure has a mix of broadline distributors and specialists, which gives it a head start over its competitors in the channel,” said Canalys Research Analyst Yi Zhang. “A mature channel strategy has allowed Microsoft to build trusted relationships between partners and customers. Working with distributors to access SMB customers, it has successfully won mindshare within the SMB market. But both AWS and Google Cloud are developing broader and deeper channel relationships in the region to support their own SMB growth.”

SMBs in APAC are taking a growing piece of the pie, showing consistent growth across the region as they are increasingly recognized for their contribution to economic growth. Estimates from Canalys show that there are roughly 60 million SMBs in this region, which represent about 55% of the IT market in APAC. This brings huge potential demand for cloud migration and adoption, but will come with challenges. Though the pandemic accelerated SMB cloud adoption, many are still slow to migrate to the cloud because of the lack of IT leadership and skills.

“Unlike enterprise customers, which have mature best-of-breed strategies, SMBs’ IT buying decisions are usually more reactive, rather than strategic or proactive,” said Canalys Analyst Sheena Wee. “Most may not have strong IT knowledge and capabilities internally, so there continues to be a strong reliance on channel partners to be trusted advisors for their IT decisions.”

Canalys defines cloud infrastructure services as services that provide infrastructure-as-a-service and platform-as-a-service, either on dedicated hosted private infrastructure or shared public infrastructure. This excludes software-as-a-service expenditure directly but includes revenue generated from the infrastructure services being consumed to host and operate them.

in Hawaii and Asia-Pacific Region")